Everything you wanted to know about structuring your house-flipping business in Ontario but were afraid to ask (because you thought it might be boring). Spoiler alert: it’s not.

Q: I’m flipping 2-3 houses a year. My neighbor says I need to incorporate. My brother-in-law says that’s overkill. My accountant just shrugged. Who’s right?

A: Ah, the classic kitchen table debate. Here’s the thing: they’re all partially right, which is why this is so confusing. Your neighbor probably heard incorporation success stories at a real estate meetup. Your brother-in-law is thinking about his cousin who flipped one house in 2022. And your accountant? Well, they shrugged because the answer is: it depends.

But let’s get specific. If you’re doing 2-3 flips annually in ontario, you’re not a hobbyist anymore. You’re running a business, whether you admit it or not. And businesses have choices.

Q: Okay, fine. I’m running a business. What are my actual options here?

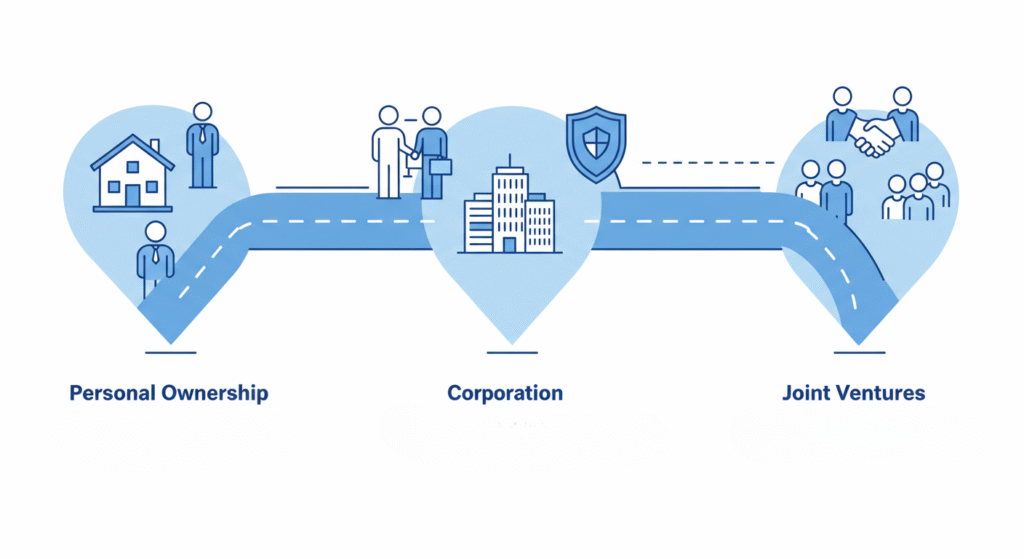

A: You have three main paths, each with its own personality:

Option 1: The “Keep It Simple” Route (Personal Ownership)

This is you, buying houses in your own name, maybe with a partner. It’s like running a lemonade stand—simple, direct, and everyone understands it.

The good news: Minimal paperwork, direct access to profits, and if you lose money (hey, it happens), you can write it off against your other income.

The less good news: You’re about to get acquainted with Ontario’s tax system in a very personal way. Every dollar of profit gets added to your regular income and taxed at your marginal rate. If you’re already making decent money, that could be 50%+. Also, if something goes sideways—a contractor sues, a buyer claims you hid foundation issues—your personal assets are on the menu.

Option 2: The “I’m Serious About This” Route (Corporation)

This is where you create a separate legal entity to buy, renovate, and sell houses. Think of it as having a dedicated business partner that handles all the property transactions and only pays 12.2% tax in Ontario.

The good news: Your corporation pays 12.2% tax on the first $500,000 of profit in Ontario (versus your personal rate of 50%+). That means more money stays in the business for the next flip. Plus, if legal trouble comes knocking, it knocks on your corporation’s door, not yours.

The reality check: More paperwork, annual filings, and your accountant will suddenly become very interested in your business. There are setup costs and ongoing compliance requirements. You’ll also need proper planning for how and when to extract money from the corporation – though with the right structure, you can maintain good flexibility for accessing your profits.

Option 3: The “Project by Project” Route (Joint Ventures)

This is like being in a band that breaks up after every album. Each flip gets its own partnership agreement.

The good news: Maximum flexibility. Want to work with different partners on different deals? Go for it. Want to bring in your rich uncle for one project? Easy.

The reality: You’ll spend more time on legal agreements than renovation plans. And you still have all the tax and liability issues of personal ownership.

Q: Everyone keeps talking about this 12.2% corporate tax rate in Ontario. That sounds too good to be true. What’s the catch?

A: The catch is that it’s not “too good to be true”—it’s just “good, but with an asterisk.”

Here’s how it really works: Your corporation pays 12.2% on active business income (the first $500,000 annually) in Ontario. But that money is now stuck in the corporation. When you eventually want to take it out and buy yourself something nice, you’ll pay personal tax on dividends.

The magic happens in the timing. Let’s say you make $50,000 profit on a flip:

- Personal ownership: Depending on your other income that year, you could pay anywhere up to the maximum personal tax rate (53.53% in Ontario in 2025)

- Corporate ownership: Corporation pays $6,100 in tax (12.2% in Ontario), leaving $43,900 for reinvestment

Even if you’re in a moderate tax bracket—say 35%—you’d still pay $17,500 personally versus $6,100 corporately. That’s an extra $11,400 available for your next project. And if you have other income pushing you into higher brackets, the corporate advantage becomes even more significant.

The tax isn’t eliminated—it’s deferred. But in business, cash flow timing is everything.

Q: I keep hearing about CRA cracking down on house flipping. Should I be worried?

A: You should be aware, not worried. CRA has definitely turned up the heat on real estate transactions, but it’s mostly targeting people who are playing games with the rules.

Here’s what changed: As of January 2023, any residential property sold within 365 days of purchase is automatically treated as business income. While certain life events like death, divorce, or employment relocation may qualify for exceptions, these circumstances are irrelevant for intentional flipping operations.

For dedicated flippers, this doesn’t change much—your profits were already business income. But it does slam the door on certain creative interpretations people used to try.

The key is proper documentation. CRA auditors are looking for people who flip houses but report the profits as capital gains (currently taxed at 50% of the gain, though this rate may increase to 66.67% starting January 1, 2026). If you’re properly structured and reporting flip profits as business income, you’re playing by the rules.

Q: My flipping partner and I split everything 50/50. How do we structure this fairly?

A: Partnership dynamics in flipping can get complicated fast. Money has a way of testing friendships.

If you go the corporate route, you’d typically form one corporation with both of you as shareholders. The split can be 50/50, or whatever reflects your actual contributions (money, time, expertise, connections).

But here’s the crucial part: Get a shareholders’ agreement. Think of it as a prenup for your business relationship. It covers what happens when:

- You disagree on a major decision

- One partner wants out

- Personal circumstances change

- The business takes off and you want to bring in other investors

I’ve seen too many successful partnerships implode because they didn’t address these scenarios upfront. As I tell my clients:

The conversation is awkward for about an hour. The lawsuit is awkward for about two years.

Q: What about liability? I hear horror stories about contractors and lawsuits.

A: The liability question is where incorporation really shines. When you own properties personally, you’re personally responsible for everything that happens. Contractor gets hurt? Your problem. Buyer discovers an undisclosed issue? Your assets are exposed.

A corporation creates a legal barrier. The corporation owns the properties, hires the contractors, and deals with any legal issues. Your personal assets—house, savings, other investments—are generally protected.

But (and this is important) incorporation isn’t a magic lawsuit shield. You still need proper insurance. You still need to follow building codes and disclosure requirements. And if you personally guarantee a loan or deliberately do something fraudulent, you can still be held personally responsible.

Think of incorporation as one layer of protection in a broader risk management strategy.

Q: I’m just starting out. Should I incorporate from day one, or wait and see how it goes?

A: This is where the “it depends” answer actually makes sense.

If you’re doing your first flip as a learning experience, starting simple might make sense. But if you’re planning to make this a real business—multiple properties, consistent activity—incorporating early has advantages.

Here’s why: transferring properties into a corporation later can trigger tax events and land transfer taxes. Starting with the right structure avoids these complications.

My general rule of thumb: If you’re planning more than one flip per year, or if your personal income is already pushing you into higher tax brackets, incorporation probably makes sense from the start.mes over. In Ontario, the difference between the 12.2% corporate rate and your personal marginal rate can save thousands per project.

Q: What about those holding company structures I keep hearing about?

A: Ah, you’ve been reading the advanced playbook. Holding companies are like the penthouse level of business structuring—useful, but not everyone needs one right away.

Here’s the concept: Instead of owning shares in your flipping company directly, you create a personal holding company that owns those shares. When your flipping company makes money, it can pay dividends up to your holding company tax-free (between connected corporations).

Why would you do this? Two main reasons:

- Asset protection: Profits moved to the holding company are further removed from the operating business’s potential liabilities

- Flexibility: More options for when and how you take money out personally

The downside? You’re now maintaining two corporations instead of one, which means double the compliance costs and complexity.

Most flippers start with a single corporation and add holding companies later as the business grows and the complexity justifies itself.

Q: Okay, I’m convinced I need professional help. But how do I find someone who actually understands real estate?

A: Not all accountants are created equal when it comes to real estate. You want someone who understands the specific rules and strategies for property investors, not just general small business accounting.

Look for someone who can discuss:

- The difference between flipping income and rental income tax treatment

- GST/HST implications for substantial renovations

- How the anti-flipping rules work in practice

- Strategies for transitioning between different investment approaches

Ask potential advisors about their other real estate clients (without expecting them to name names). Do they work with other flippers? Property developers? Rental property owners? Experience matters in this specialized area.

Q: Bottom line: What should I do?

A: Here’s the thing about tax and business structure advice: anyone who gives you a definitive answer without understanding your specific situation is probably wrong.

But here’s what I can tell you: if you’re serious about fix-and-flip investing in Ontario—whether you’re in Toronto’s competitive market or finding deals in London or Hamilton—the structure you choose will significantly impact your success.

The difference between optimal and suboptimal structuring can easily be $20,000-$50,000+ annually in tax savings alone, depending on the number of properties and profit levels. For active flippers doing multiple high-value projects, the savings can be even more substantial. Over a few years, that’s life-changing money.

Don’t let analysis paralysis stop you from getting started, but also don’t let simplicity stop you from optimizing. The real estate market in Ontario is competitive enough without giving away profits to poor tax planning.

Would you like more help?

That’s normal. Real estate investing is complicated, and every situation is unique.

If you have further questions or would like to discuss your particular circumstances in detail and seek some tailored tax advice, you can book a 25-minute strategy session below.

This Q&A provides general information and should not be considered specific tax or legal advice. Tax laws change frequently, and every investor’s situation is unique. Always consult with qualified professionals before making structure decisions.